Accept crypto donations

Set up crypto donation platform in order to receive crypto donations. Add crypto as a donation method on your website with just a few clicks.

·One-click activation·

·Secure processing·

·Flexible integrations

·One-click activation·

·Secure processing·

·Flexible integrations

Trusted by the world’s top nonprofits

4.8/5

4.8/5

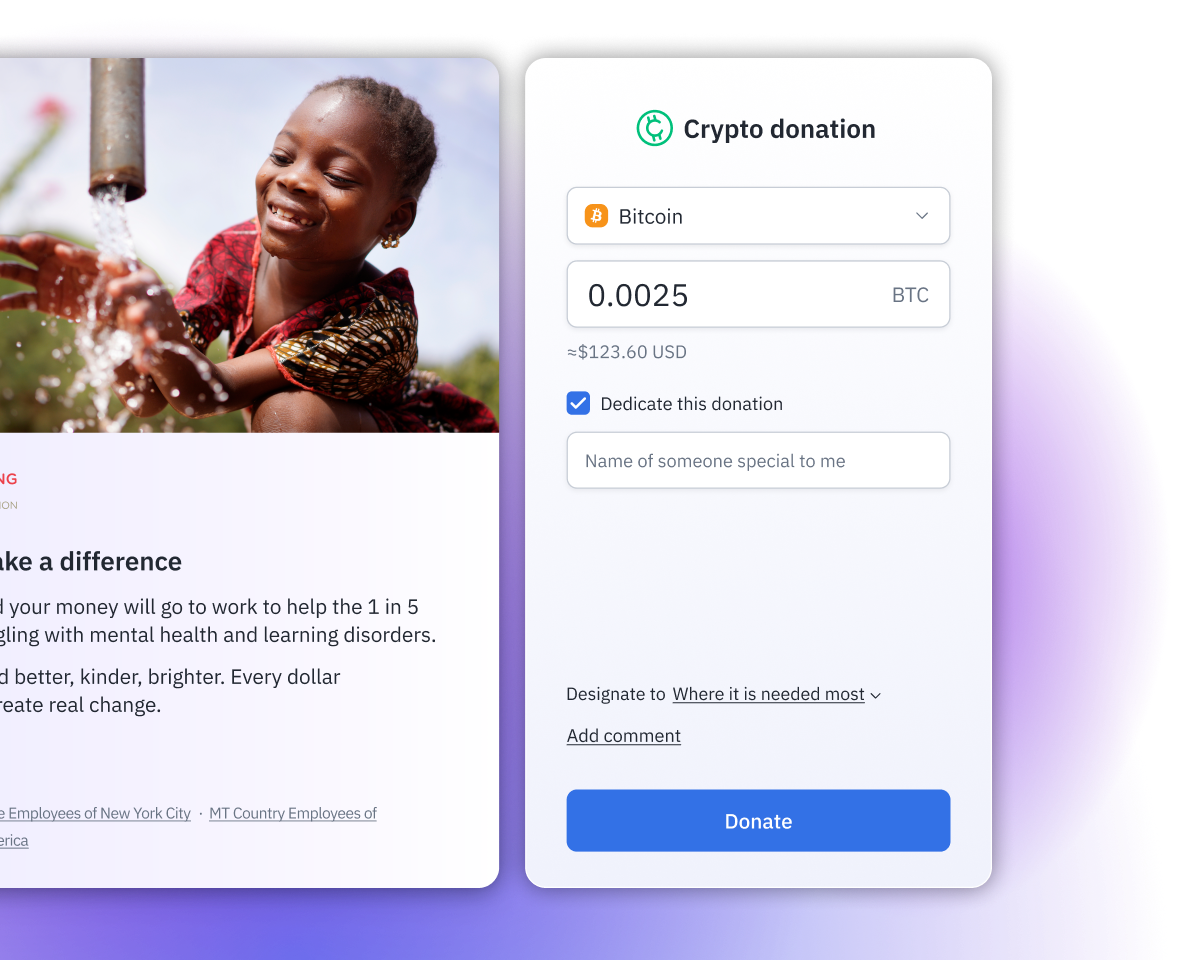

Accept crypto donations through your website

Start accepting crypto donations with just a few clicks. With Fundraise Up, crypto giving is integrated with your existing website and other payment methods.

Explore Payment methods

Secure donations that average $10K in size

Unlock a new way for ultra-generous donors to support your mission. Enable crypto giving to capture gifts worth 142 times more than standard currency donations.

Read crypto guide

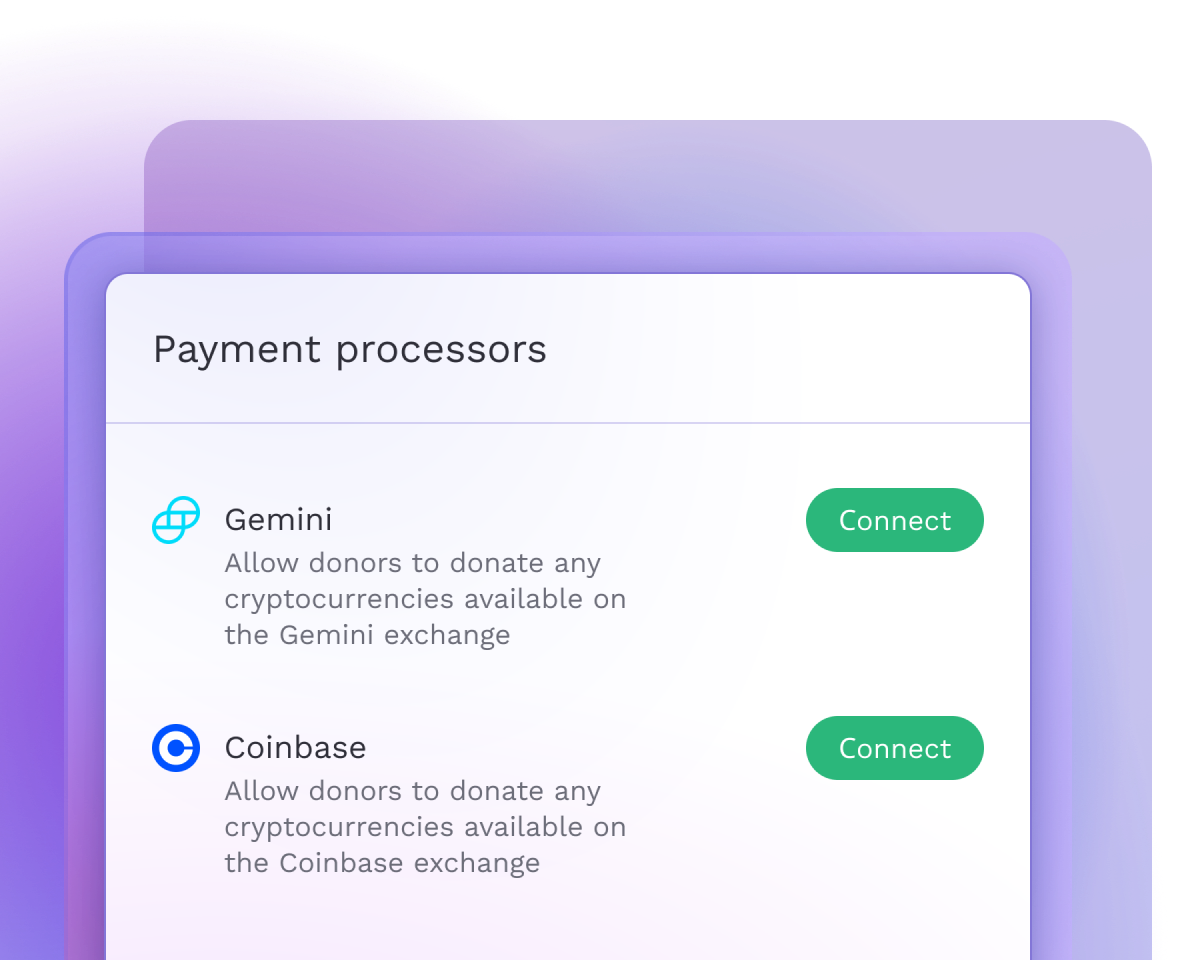

Connect your own crypto exchange account

Get the flexibility and control of a bring-your-own-account model. Connect a crypto exchange account that your nonprofit owns and manages.

See exchange comparison

Security

See Fundraise Up’s comprehensive security tools and compliances that safeguard your nonprofit and donors.

Explore Security

Start accepting crypto donations today!

Talk to our sales team to learn more and get pricing.

Request a demo